")

Trade Hero Weekly Research Report

Week of 4

Stock Pick of the Week: DXP Enterprises (NASDAQ: DXPE)

Current Price

$85

Sector

Industrial Solutions

Revenue Growth

12.8% YoY

Dividend Yield

None

Revenue Growth

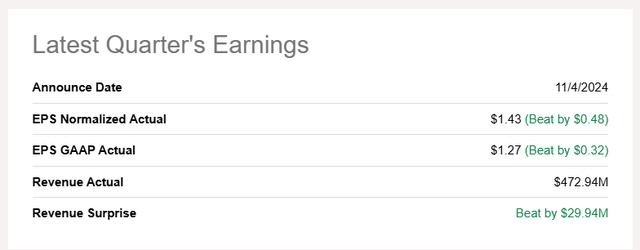

Previous Earnings Report

Overview of Operations:

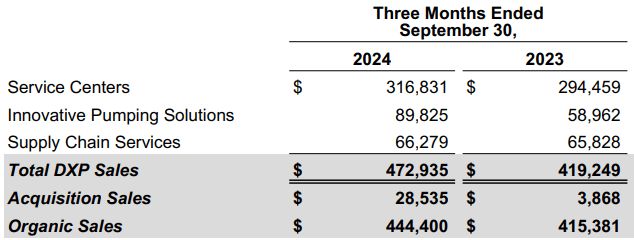

DXP Enterprises (DXPE) specializes in providing industrial solutions with a focus on distribution, maintenance, repair, and overhaul services. Its three main business segments are:

1. Innovative Pumping Solutions (IPS): Offers custom-designed pumping systems for industrial, municipal, and energy clients. This segment drives high-margin growth and has seen significant gains due to wastewater and energy-related projects.

2. Service Center (SC): Provides maintenance, repair, and operational supplies, along with U.S. safety services and metalworking products. This division has rebounded strongly after a challenging start in 2024.

3. Supply Chain Services (SCS): Delivers integrated supply chain solutions, benefiting from new accounts and technological improvements, though growth in this segment has been relatively slower.

Sector Outlook:

The industrial solutions sector is poised for robust growth, driven by increasing infrastructure investments, water and wastewater projects, and the ongoing global energy transition. DXP Enterprises is well-positioned to capitalize on these trends due to its expertise in niche markets and strategic acquisitions. The company’s focus on higher-margin businesses aligns with the industry's move toward value-added services.

Upcoming Catalysts:

1. Elevated Backlog: Strong order bookings for energy and wastewater projects support revenue growth in 2024 and beyond.

2. Acquisition Strategy: DXPE has completed seven acquisitions year-to-date and expects two more by Q1 2025, contributing significantly to topline growth.

3. Strategic Expansion: Investments in capacity and operational capabilities, particularly in the IPS segment, should bolster margins and revenue.

Performance Highlights:

Q3 2024 Revenue: $472.9 million, reflecting a 12.8% year-over-year growth.

EBITDA Margin: Improved to 11.1%, supported by contributions from high-margin acquisitions.

Stock Valuation: Trades at a forward P/E of 19.38, below its five-year average of 22.14, indicating potential upside for investors.

Why DXPE?

Despite a recent stock rally, DXPE remains undervalued compared to industry peers and historical levels. The company's consistent growth, focus on high-margin segments, and disciplined acquisition strategy make it a great buy for our investing strategy to gain exposure to the industrial sector.

Key Metrics

Revenue Growth

12.8% YoY

EBITDA Margin

11.1%

Backlog

Strong

Investment Strategy

DXP Enterprises offers a compelling opportunity for growth-oriented investors. Consider these strategies:

- Buy on Fundamentals: Leverage DXPE's undervalued status compared to peers and historical averages.

- Focus on Long-Term Growth: Position for multi-year gains driven by strategic acquisitions and market expansion.

- Monitor Key Segments: Track IPS and Service Center performance for continued topline growth.